With tight schedules, a limited personal history with patients, disparities in local resources, and a litany of cost-control measures established by insurers, even hospitalists in the know concede that helping Medicare patients manage drug costs can be an exercise in frustration. As a result, patients are often left with medications that require higher cost-sharing or aren’t even on a plan’s formulary, forcing them to pay out-of-pocket for a prescription. Adding insult to injury, any money spent on a medication not covered by a Part D plan doesn’t count toward getting a patient out of the doughnut hole.

click for large version

click for large version

The Extra Mile

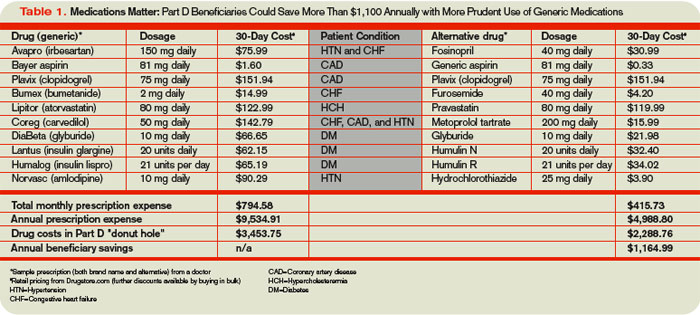

Jocelyne Watrous, a Medicare beneficiary consultant at the Willimantic, Conn.-based Center for Medicare Advocacy, says drug affordability while in the doughnut hole is a hardship for many. But so are specialty drug copays that range from 25% to 33% of the total price (see Table 1, below). For expensive prescriptions, Watrous says, hospitalists can get the name of a patient’s Part D formulary from the membership card and check for restrictions, such as prior authorization, quantity limits, or step therapy. “This is a terrible burden to place on physicians and their staffs, but nothing is worse than having the patient come back to the hospital via the ER because they could not get the drug prescribed by their doctor,” she says. “Best to square it all away before discharge, if possible.”

Brandon Koretz, MD, an associate clinical professor of geriatric medicine at the University of California at Los Angeles, says keeping track of differences among the dozens of Part D plans isn’t feasible. “Oftentimes, what happens is, you find yourself writing a prescription for what you think is a reasonable and cost-effective treatment, only to find out that drug A is not on insurance company B’s formulary, but drug C is,” Dr. Koretz says.

And if doctors are confused by the array of Part D formularies, hospitalists wonder, how can geriatric patients be expected to navigate the system, especially given the not-insignificant number with cognitive impairments?

Bill Vaughan, a health policy analyst for Consumers Union in Washington, D.C., compares the consumer paralysis created by the proliferation of prescription drug plans to walking by a store display featuring 20 brands of jam. “You’re kind of awed by it, but you don’t buy anything because you’re kind of intimidated,” he says. Only instead of 20 varieties, the typical local government agency offered 48 competing Part D plans in November 2006, with some boasting more than 70. In a new study sponsored by the Henry J. Kaiser Family Foundation, Massachusetts Institute of Technology economist Jonathan Gruber found that when seniors made a decision, only 6% to 9% chose the least expensive plan, while the remaining seniors paid an extra $360 to $520 annually (www.kff.org/medicare/7864.cfm).

All too often, economic problems are simply transferred to other providers. Nursing home pharmacists have complained to Dr. Zerzan about doctors switching seniors’ medications to hospital formulary drugs that aren’t covered under Part D, requiring pharmacists to switch the drugs back again. “From their standpoint, it takes a ton of work because hospitalists don’t know what’s on their formulary,” she says.

Miscommunication can wreak havoc in other ways. Dr. Zerzan recalls how her parents were hosting her grandmother in Oregon when she fell and broke her pelvis. At the hospital, she arrived with two overlapping medication lists from her primary-care physician, cardiologist, and rheumatologist in California. The lists contained several combination pills that essentially duplicated her cholesterol and blood pressure medications. Instead of conducting a medication review, the hospital left the lists intact and added its own, sending her grandmother home with a “fistful of prescriptions.” Unsurprisingly, her blood pressure dipped dangerously. “She actually ended up going back into the hospital briefly to sort out her medications because it was such a mess,” Dr. Zerzan says.